[ad_1]

[ad_1]

A person retirement account, or IRA, is a tax-advantaged funding account that lets you save for retirement on both a tax-free or tax-deferred foundation, relying on the sort of account you might have.

With a standard IRA, you will not pay taxes in your earnings till you make a withdrawal in retirement, or you'll be able to contribute after-tax earnings with a Roth IRA. Each of those sorts of accounts may help fund your retirement, maybe alongside Social Safety funds and office advantages akin to a 401(ok).

No matter what IRA you select, these accounts can enhance your retirement saving and diversify your portfolio. We'll clarify the variations between the 2 principal kinds of IRAs under.

IRA quick information:

-

- Anybody can open an IRA account so long as they've earned earnings, even minors.

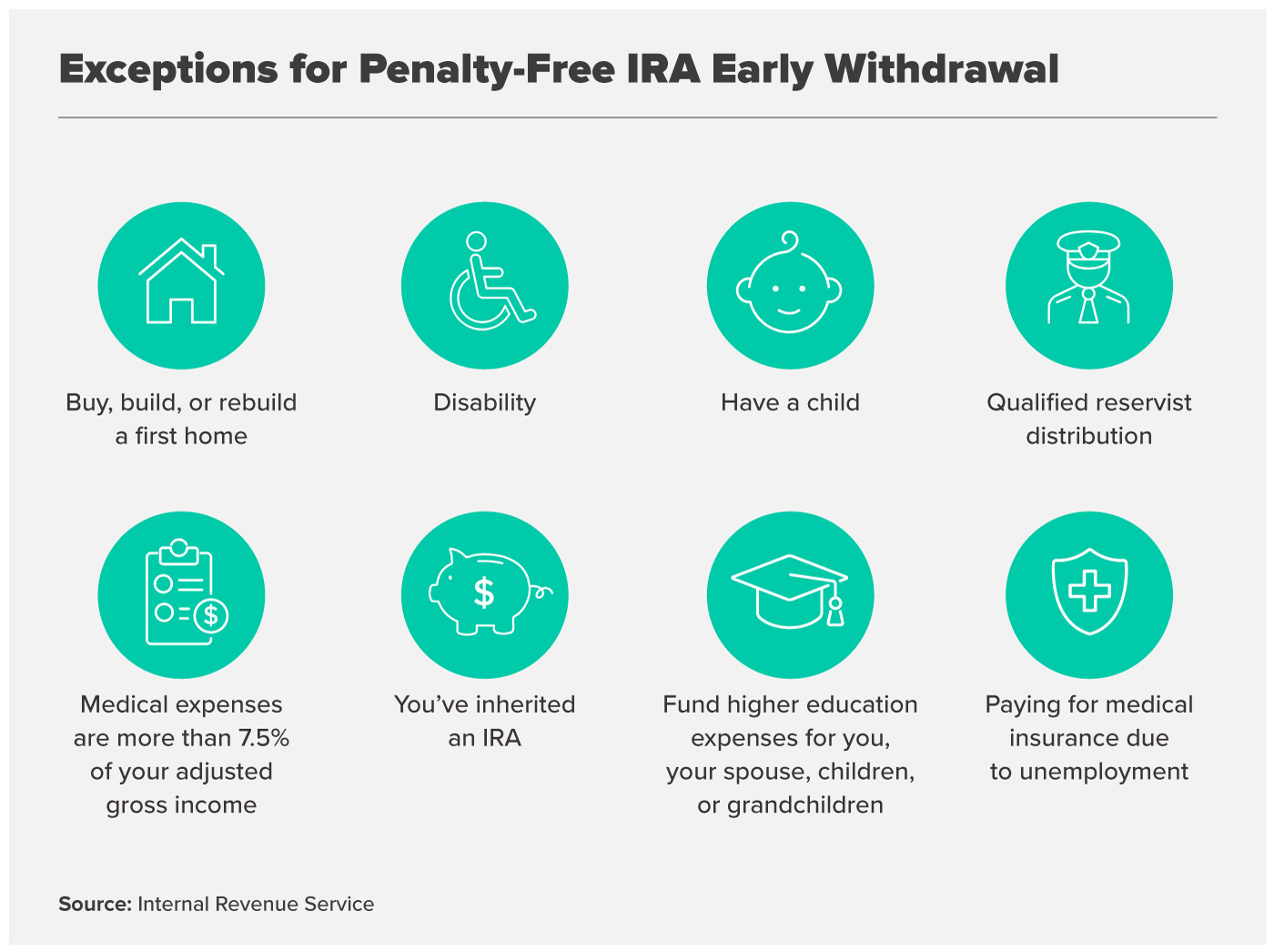

- There are particular exceptions that enable for penalty-free early withdrawals of your IRA contributions.

- Typically, nonetheless, withdrawing earnings earlier than the age of 59½ is topic to a ten% tax penalty.

- You may personal multiple kind of IRA.

- Anybody can open an IRA account so long as they've earned earnings, even minors.

- There are particular exceptions that enable for penalty-free early withdrawals of your IRA contributions.

- Typically, nonetheless, withdrawing earnings earlier than the age of 59½ is topic to a ten% tax penalty.

- You may personal multiple kind of IRA.

A part of what makes IRAs engaging is that they're easy to arrange and supply sure tax advantages. In contrast to a 401(ok), which requires sponsorship from an employer, you'll be able to open an IRA via a financial institution, dealer or an automatic funding advisor by yourself in minutes. There isn't any age requirement on these accounts, so anybody can open an one so long as they've W-2, 1099, or 1040 earnings.

Figuring out what kind of IRA is best for you relies on your earnings, each now and what you anticipate to earn sooner or later. Roth IRAs have an earnings restrict of $161,000 for single filers and $240,000 for married couples submitting collectively as of 2024. In case your wages surpass the cap, you might need to contemplate a standard IRA.

In accordance with Alicia Munnell, director of the Center for Retirement Research at Boston College, should you’re eligible for each a Roth and a standard IRA, it is best to check out your tax expectations sooner or later to resolve the neatest possibility.

“If you have a high income, a traditional IRA can allow you to defer paying income tax now and help you save toward retirement," Munnell says. "If you would prefer to pay taxes upfront as you contribute and not worry about it later, a Roth can be a good investment.”

Conventional vs. Roth IRAs

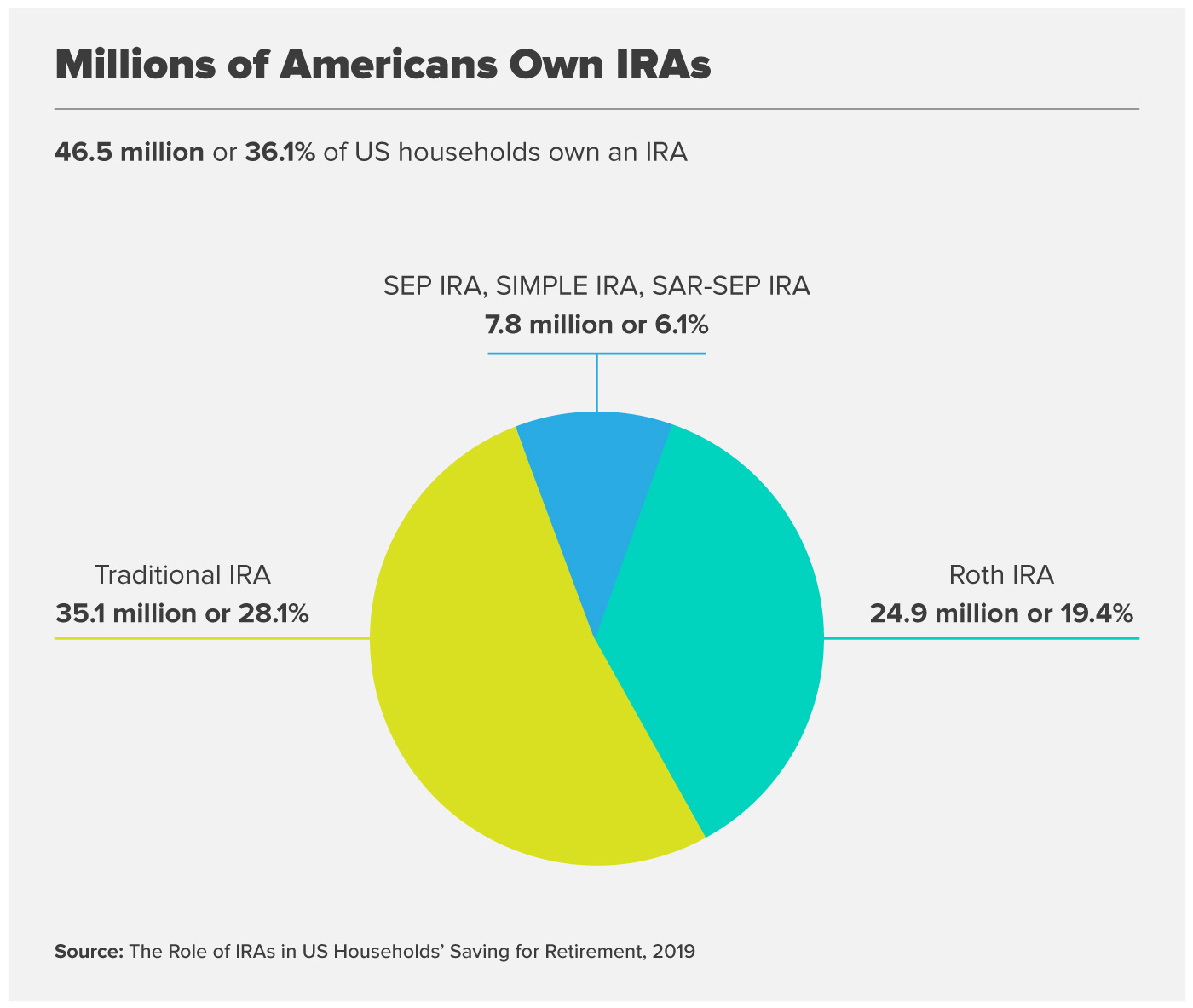

Conventional and Roth IRAs are the commonest IRAs. Greater than 60 million Individuals personal IRAs as of 2020, in line with the assume tank Tax Policy Center, with the common account steadiness hovering round $157,000.

One of many principal benefits of each conventional and Roth IRAs is that your investments will develop tax-free.

| Conventional IRAs vs. Roth IRAs |

| You may defer paying earnings tax in your contributions till they're withdrawn out of your account. | Your investments are made with after-tax dollars so that when you attain retirement you’ll get your financial savings tax-free. |

| Has no earnings restrict. | Has an earnings restrict. |

| Has required minimal distributions (RMDs) beginning at a selected age. The account holder should begin taking RMDs at 72, or at 73 in the event that they flip 72 after Dec. 31, 2022. | Has no required minimal distributions (RMDs,) which means you'll be able to proceed to let your financial savings develop indefinitely. |

| Chances are you'll qualify for a tax deduction. | Doesn’t embrace tax breaks. |

| There’s a ten% early withdrawal penalty on distributions earlier than age 59½ until the cash is withdrawn attributable to an exception akin to loss of life, incapacity, funding schooling, medical bills, a primary house buy, or the delivery or adoption of a kid. | Withdrawals are extra versatile. For one, you'll be able to withdraw contributions any time with out penalty, since you've got already paid taxes. As for withdrawals on earnings, they're tax-free should you’ve had a Roth IRA for at the very least 5 years and you're 59½ (or older). You too can withdraw tax-free at any age should you’ve had a Roth IRA for 5 years and qualify for sure exceptions, akin to a first-home buy. |

| Similarities |

| You may develop money tax-free. |

| You may open an account no matter your age, so long as you might have earned earnings. |

| You may contribute as much as $7,000 in 2024 ($8,000 should you’re 50 or older), even should you’re additionally contributing to a 401(ok) or different company-sponsored financial savings account. |

What sort of IRA is correct for me?

If you happen to’re one of many many individuals considering of beginning a retirement financial savings account, it’s vital to discover all your choices. Opening an IRA is straightforward, and most of the people spend money on them to make the most of their tax advantages, which assist their cash develop sooner.

There are just a few different kinds of IRAs along with the standard and Roth, and every one has its benefits. This is a breakdown of the totally different IRAs accessible to customers:

| Kind of IRA | Definition | Contribution restrict |

| Conventional IRA | A conventional IRA permits your contributions to develop tax-deferred till you withdraw them upon retirement. There are two principal kinds of conventional IRAs: deductible and nondeductible. Your monetary scenario will decide whether or not or not you get a tax deduction in your contribution. Non-deductible IRAs are much like Roth IRAs in that contributions are made with after-tax dollars, however differ from them in that contributions aren’t restricted by how a lot you earn. | For 2024, whole annual contributions to your conventional IRA can’t exceed $7,000 ($8,000 should you’re age 50 or older). Your contributions can’t surpass your taxable compensation for the 12 months. |

| Roth IRA | A Roth IRA is funded with after-tax dollars, which means you’ve already paid taxes on the cash you set into it. In return, your cash grows tax-free. When you retire and withdraw your financial savings, you gained’t pay any taxes. | For 2024, whole annual contributions to your Roth IRA can’t exceed $7,000 ($8,000 should you’re age 50 or older). Your contributions can’t surpass your taxable compensation for the 12 months. |

| SEP IRA | A SEP IRA (or Simplified Worker Pension) is a sort of conventional IRA designed for self-employed people and small enterprise homeowners with few staff. Like conventional IRAs, the cash in SEP IRAs will not be taxable till withdrawn. In contrast to conventional IRAs, these are funded with employer contributions solely. | Contributions for tax 12 months 2024 could be as much as 25% of compensation or as much as $69,000, whichever is much less. |

| SIMPLE IRA | In contrast to SEP IRAs, staff are allowed to contribute to a SIMPLE IRA (or Financial savings Incentive Match Plan for Staff). SIMPLE IRAs are mostly utilized by small enterprise start-ups with beneath 100 staff. Moreover, employers are required to match as much as 3% of the worker’s wage or make nonelective contributions of two%, as much as an annual restrict of $290,000 for 2021. | Staff can contributes as much as $16,000 from their wage to a SIMPLE IRA in 2024, plus a catch-up contribution of $3,500 for these over 50. |

| Spousal IRA | Spousal IRAs are supposed for married couples and permit the working partner to contribute to an account on behalf of a partner that earns little or no earnings. To qualify for a spousal IRA, couples should file their earnings taxes collectively. It’s value noting that spousal IRAs are usually not co-owned. | Every partner could contribute as much as the identical restrict as conventional IRAs or Roths ($7,000 for 2024). Nevertheless, the full of their mixed contributions can’t exceed the taxable compensation reported on their joint earnings tax return. |

Who can open an IRA?

You need to have earned earnings from a W-2 job or self-employment to open an IRA, which suggests nearly anybody with a job can open an IRA account, no matter age.

A dad or mum or authorized guardian can arrange an IRA for a minor via a custodial account. As soon as minors flip 18, or 21 in sure states, they are going to have full entry to their IRA account.

Sorts of IRA rollovers

An IRA rollover — generally known as a "rollover IRA" — lets you transfer cash out of your former employer-sponsored retirement plan to an IRA. Many individuals roll over their financial savings to consolidate former employer 401(ok) plans and keep away from the trouble of early withdrawal tax penalties.

Nevertheless, there are some components it is best to be careful for when rolling over your IRA. If achieved incorrectly, your rollover might be thought-about a distribution or early withdrawal and be topic to taxation.

Larry Sprung, founder and wealth advisor at Mitlin Monetary, says there are two strategies to keep away from potential pitfalls.

“The easiest and least troublesome option is a direct rollover. With a direct rollover, you have the custodian of the current IRA write a check to the custodian of the new IRA for your benefit. And you as the IRA holder never take possession of the money,” Sprung says.

The second methodology is an oblique rollover, which can present a verify to your title that have to be deposited inside 60 days after you obtain it. If you happen to fail to take action, the cash can be fully taxable. You additionally have to be sure you're not choosing the choice to withhold taxes once you full the oblique rollover utility.

“If you withdraw money from a 401(k), the default is to withhold 20% for tax purposes, it’s very common for people to make the mistake of inadvertently withholding taxes unless they specify otherwise,” Sprung says.

Whereas the IRS permits just one oblique rollover in any 12-month interval, there isn't a restrict to the variety of direct rollovers you'll be able to request.

“If you happen to're trying to rollover cash and it isn't a direct rollover, you actually need to seek the advice of a wealth advisor, monetary advisor or your CPA to just remember to're filling out that paperwork correctly," Sprung provides.

Relying on the plan you might have, your investments may preserve their tax-deferred standing when rolled over instantly into an IRA account. Some certified plans embrace 401(ok), cash buy, profit-sharing and outlined advantages plans. If you happen to're contemplating a Rollover IRA, confirm whether or not your account qualifies for a rollover.

Look ahead to early withdrawal tax penalties

You may withdraw early from an IRA previous to age 59½, however the cash could also be included as a part of your gross earnings and topic to a ten% further tax penalty. Nevertheless, tax penalties are waived in case your early withdrawal is for a qualifying distribution, or should you meet sure exceptions.

How do I open an IRA?

You may open an IRA account via quite a lot of monetary establishments, together with online banks.

Earlier than getting began, take your time evaluating suppliers. Whereas the IRS doesn’t require a minimal contribution to get an account began, some suppliers could require $500 to $1,000 as an preliminary deposit plus servicing charges, relying on the account. Different establishments could have a decrease minimal deposit requirement or none in any respect, so weigh your choices.

0 Comments